Accounting Services Phuket: +66 (0) 76 510 111

Tax Payment Schedule in Thailand

The taxpayer in Thailand should file a Personal Income Tax Return (PIT) and make payment to the Revenue Department within the last day of March of the following tax year. For taxpayers who derive their income as per category (5) – (8) during the first six months of the taxable year, they should file their half-year return and make payment to the Revenue Department within the last day of September of the tax year. Withholding tax or half-year tax that has already been paid can be used as credits against the tax liability at the end of the year.

Personal Income Tax

Tax computation for Personal Income Tax follows:

Taxable Income = Assessable Income – deductions – allowances

where,

Individual taxpayers may seek the assistance of a reliable accounting service Phuket in the preparation, filing, and payment of the personal income tax.

Corporate Income Tax

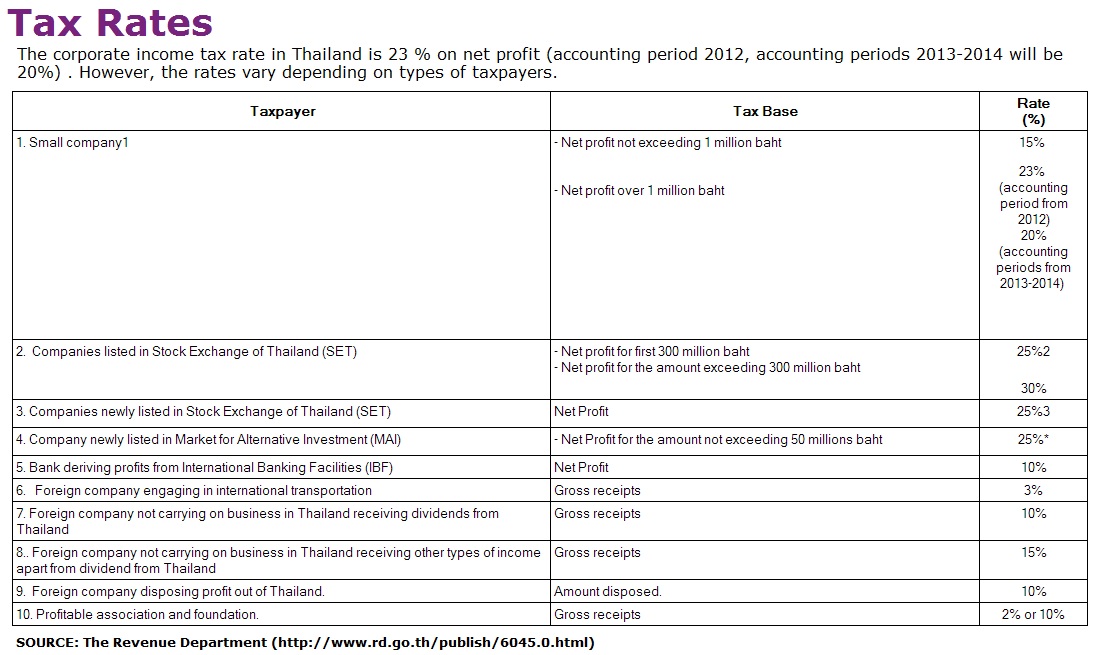

Companies and partnerships established under the laws of Thailand are subject to income tax on income earned from sources within and outside the country via the Corporate Income Tax. Corporate Income Tax is imposed on the net profits as per the generally accepted accounting principles and according to the conditions specified in the Thailand Revenue Code. Tax planning Phuket service providers can provide assistance in preparing, filing and payment of the corporate income tax with the Revenue Department.

The Corporate taxpayer should know that:

Specific Business Tax

This tax is imposed on businesses involved in banking, finance, life insurance, pawnshops, and real estate. These businesses not included in the VAT system. Specific business tax is computed on monthly gross receipts which do not include municipal tax.

Municipal Tax in Thailand

Municipal tax is paid at the rate specified by the government when specific business tax is paid. When VAT is paid, one-ninth of its rate goes to municipal tax.

Customs Duty

This tax is mainly imposed on import and some export goods specified in the Customs Tariff statute. In general, the basis for tax computation is the invoice price and it’s normally applied to CIF (Cost, Insurance, and Freight) value for import and FOB (Free On Board) for export. Exported goods that are subject to customs duty include rice, rubber, leather, and teak.

Thai Company. A Thai company generally pays tax at 30% of net profit. However, some types of company are entitled to a rate reduction.

Foreign Company. A foreign company carrying on business in Thailand, whether it has a branch, an office, an employee or an agent in Thailand shall pay 30% tax only on profit deriving from business in Thailand. However, international transportation company shall pay tax at the rate of 3% on gross receipts. To give you a view on how much tax expats pay, you can look at this article.

Foreign Company Abroad. A foreign company that does not carry on business in Thailand will be subject to withholding tax on certain categories of income derived from Thailand. The withholding tax rates may be further reduced or exempted depending on types of income under the provision of Double Taxation Agreement.

You must be logged in to post a comment.